NO.PZ2020021203000078

问题如下:

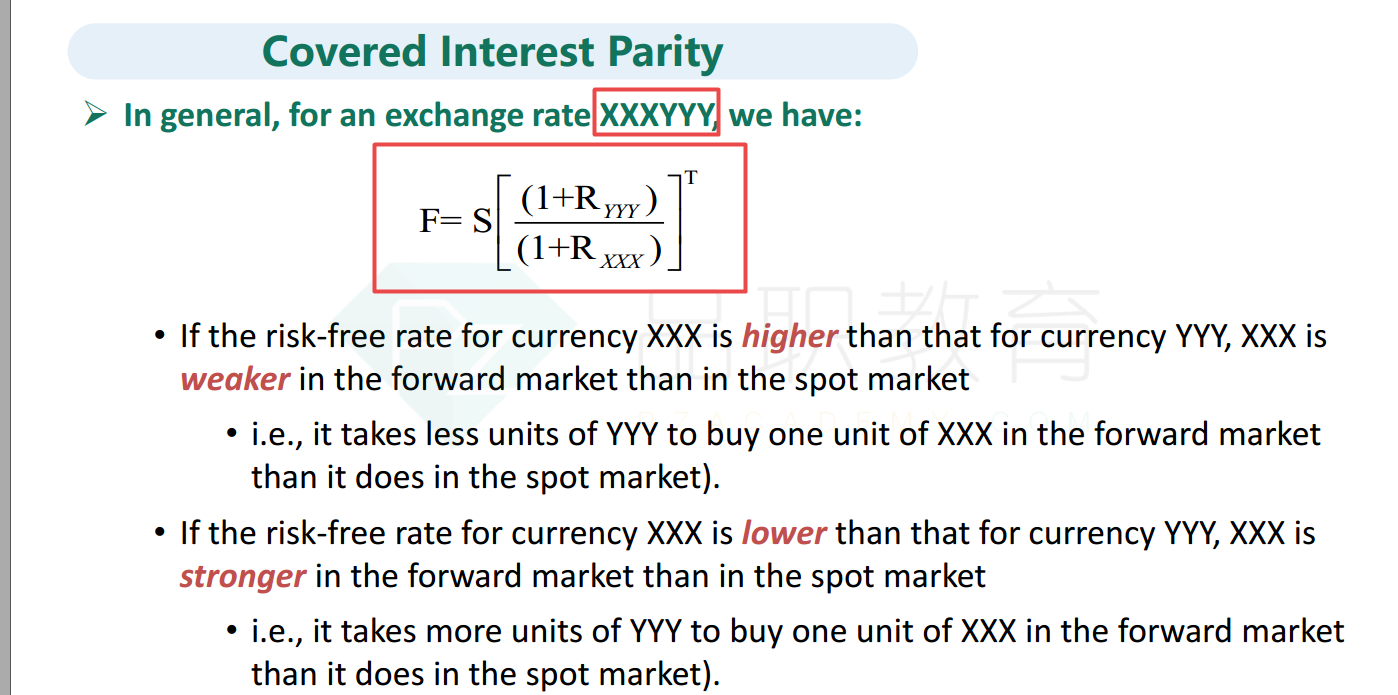

Use the results in Chapter 9 to determine put-call parity for a currency options on the GBP/USD exchange rate. Express your answer in terms of the USD risk-free rate, RUSD, the GBP risk-free rate, RGBP, and the time to maturity, T.

选项:

解释:

with equation

Substituting this into Equation Price + PV(K) = European Put Price + PV(F) and noting that:

European Call Price + = European Put Price +

老师,1.GBP/USD,利率平价公式的分子不是GBP的利率吗?有一点晕。

2.能用画图法讲解一下吗?谢谢。