NO.PZ2020011303000190

问题如下:

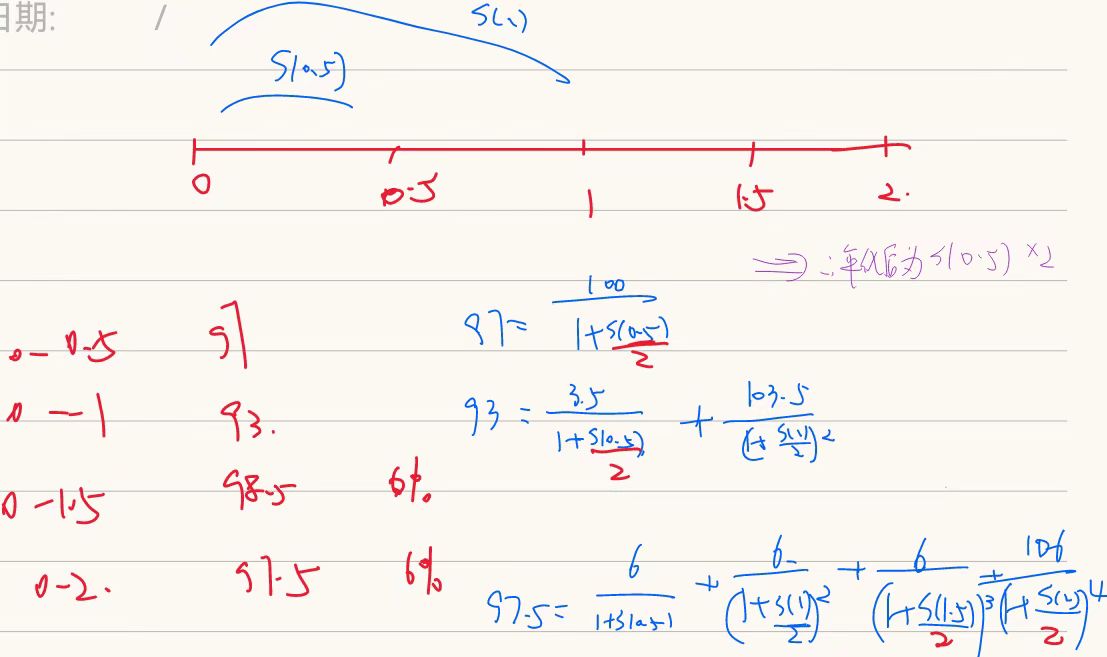

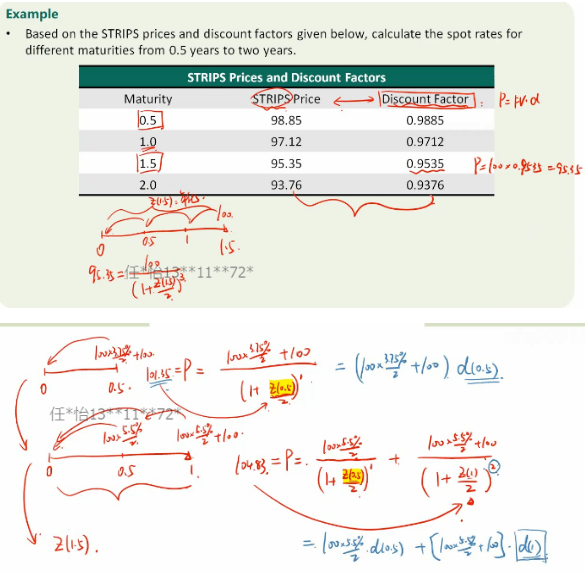

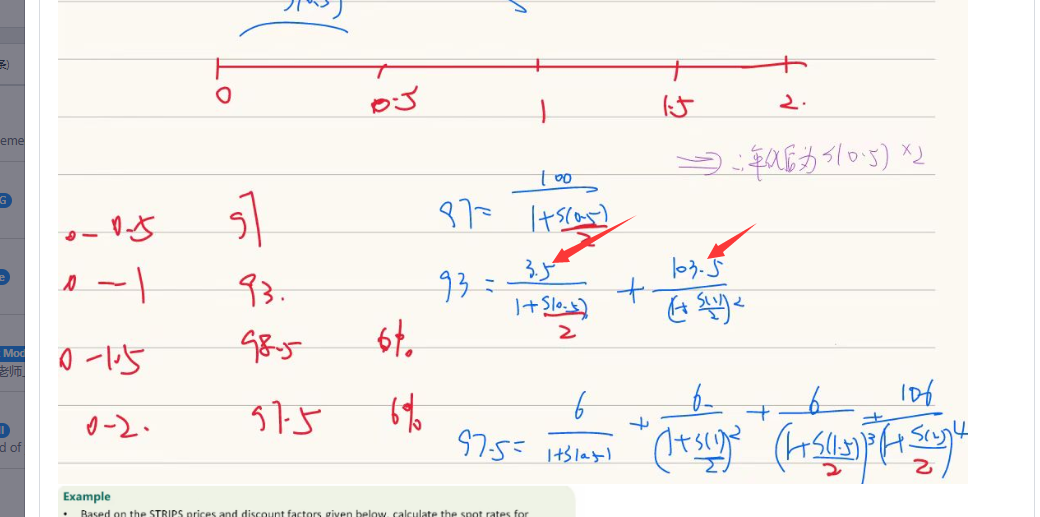

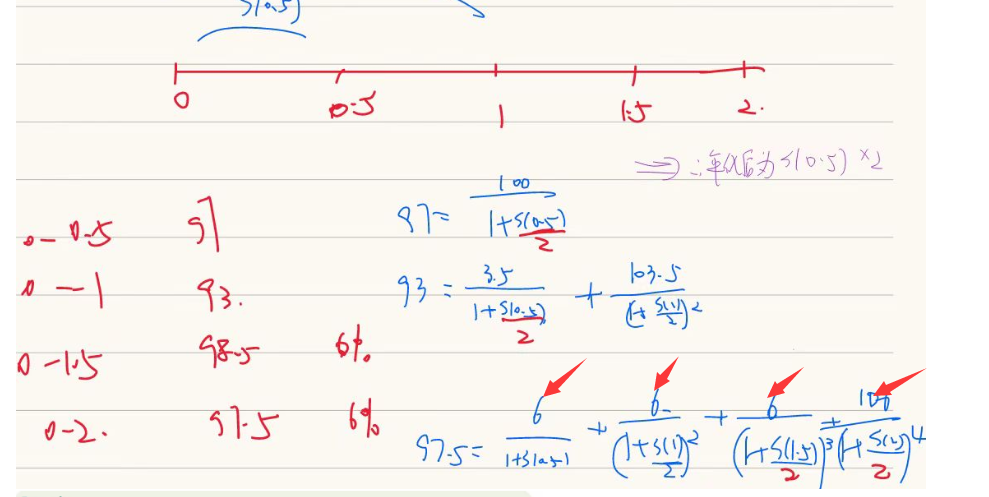

The cash prices of 6-month and one-year Treasury bills are 97.0 and 93.0. A 1.5-year and two-year Treasury bond with coupons at the rate of 6% per year sell for 98.5 and 97.5. Calculate the six-month, 12-month, 18-month, and 24-month spot rates with semi-annual compounding.

选项:

解释:

1. The six-month rate (semi-annually compounded) is 2 x (100/97-1) = 0.06186 or 6.186%.

2. The one-year rate (semi-annuallycompounded) is 2 × [ (100/93)1/2-1 ] = 0.07390 or 7.390%.

3. The coupons on the 1.5 year bond have a value of 0.97 × 3 + 0.93 × 3 = 5.7.

The value of the final payment is therefore 98.5 − 5.7 = 92.8.

The discount factor for 1.5 years is 92.8/103 = 0.900971.

This corresponds to a spot rate (semi-annually compounded) of 7.074%.

4. The coupons on the two-year bond have a value of

The value of the final payment is therefore 97.5 – 8.4029 = 89.0971.

The discount factor for two years is 89.0971/103 = 0.8650.

This corresponds to a spot rate

(semi-annually compounded) of 7.383%.

题目问:6个月和1年的T-bill的价格是97和93,1.5年和2年的T-bond,coupon rate是6%

per year价格是98.5和97.5,计算6个月、12个月、18个月、24个月的半年付息一次的spot rate是多少?

1. 6个月的spot

rate(半年付息一次)= 2 x (100/97-1)

= 6.186%

2. 1年的spot rate(半年付息一次)= 2 × [ (100/93)1/2-1 ] = 7.390%

3. T-bond是附息债券,T-bill是零息的,T-bill求出来的价格就是折现系数,6个月的折现系数是0.97,12个月的折现系数是0.93

1.5年期的附息债券的coupon的价格= 0.97 × 3 + 0.93 × 3 = 5.7.

最后一笔本金的价格=98.5 − 5.7 = 92.8.

1.5年的discount factor= 92.8/103 = 0.900971

discount factor=1/(1+r)^n

即可反求出:1.5年的spot rate(半年付息一次) =7.074%.

4. 2年期的附息债券的coupon价格=3 × 0.97 + 3 × 0.93 + 3 × 0.900971 = 8.4029

最后一笔本金的价格=97.5 – 8.4029 = 89.0971

2年的discount factor= 89.0971/103 = 0.8650

discount factor=1/(1+r)^n

即可反求出:2年的spot rate(半年付息一次) =7.383%.