NO.PZ202207040100001002

问题如下:

Which of Parker’s statements about Manager B in Exhibit 1 is most appropriate? The statement about:选项:

A.tracking errors. B.excess return. C.currency overlays.解释:

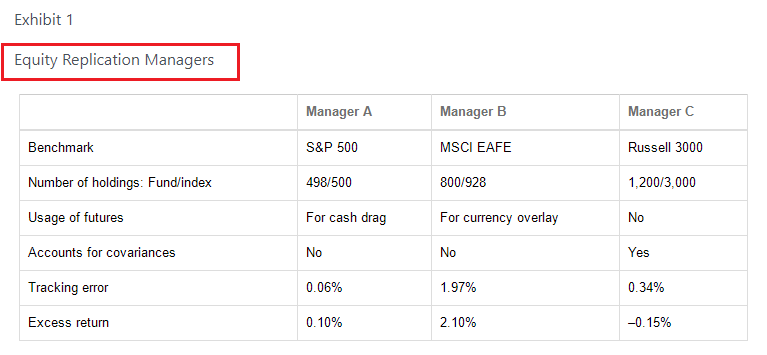

SolutionB is correct. The comment about excess return being luck rather than skill is correct. Replication managers attempt to create a portfolio that tracks the performance and the volatility of the underlying index as closely as possible. The proper measure of skill is the tracking error: Manager B has the highest tracking error among the three managers.

A is incorrect. Tracking error does not measure volatility of the portfolio; rather, it measures the volatility of the excess return between the index and the portfolio.

C is incorrect. A currency overlay assists a portfolio manager in hedging (not levering) the returns of securities that are held in foreign currency back to the home country’s currency.

请问老师,tracking error越大, excess return越归因于幸运?