NO.PZ202206260100000502

问题如下:

What would the rationale most likely be for an institutional investor to include the Pegasus Fund in its portfolio?

选项:

A.Uncorrelated source of alpha

B.Capital structure arbitrage of valuation divergence

C.Earn the illiquidity premium associated with the strategy

解释:

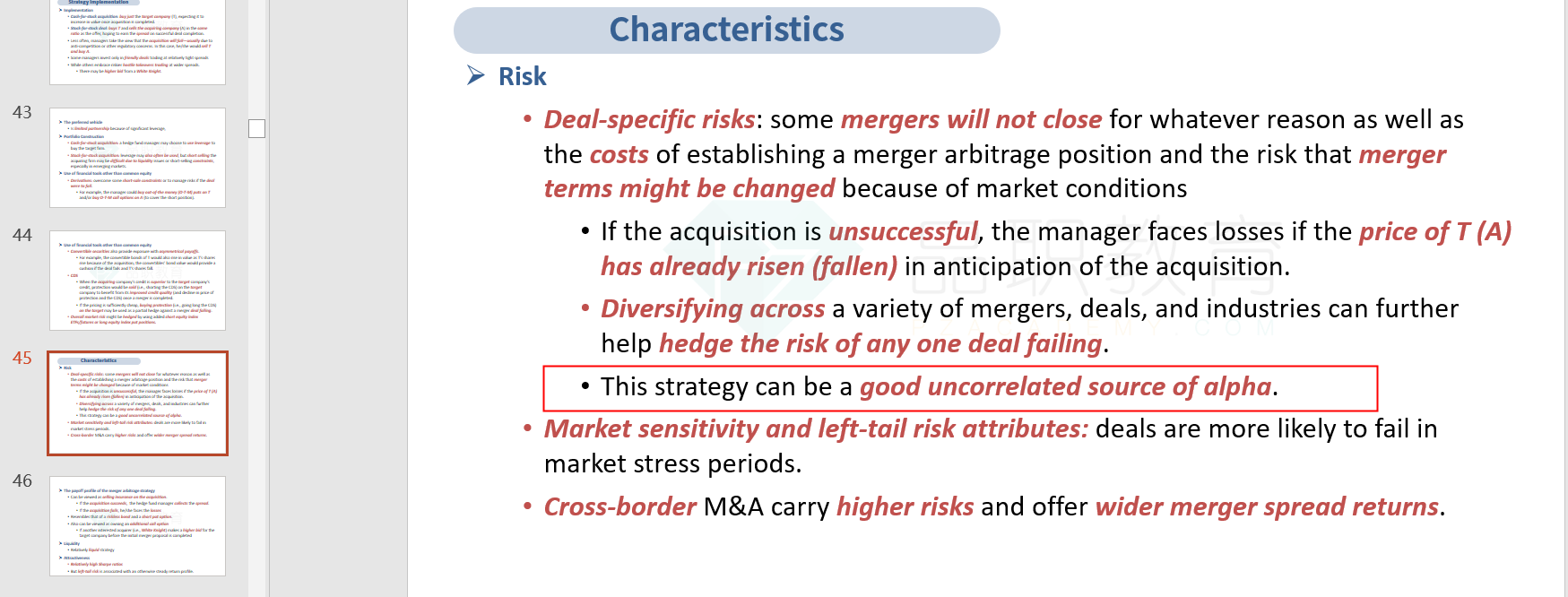

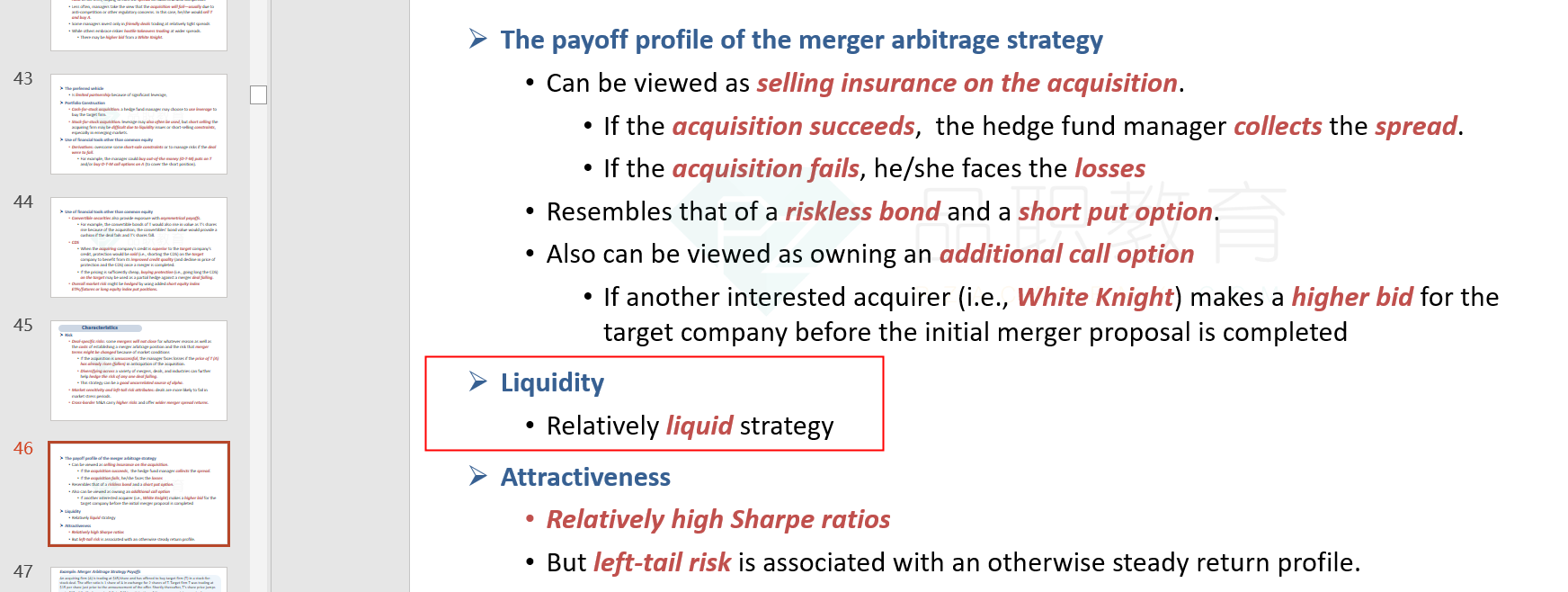

SolutionA is correct. Merger arbitrage is a good uncorrelated source of alpha. Diversifying across a variety of mergers, deals, and industries can further help hedge the risk of any one deal failing. Merger arbitrage does not exploit capital structure divergence in a single company and is a relatively liquid strategy.

B is incorrect because capital structure arbitrage involves taking long and short positions in the debt and equity of individual companies to extract misvaluations, and it would not be a rationale for inclusion in the portfolio. This generally falls under distressed security strategies.

C is incorrect because merger arbitrage is a liquid strategy.

这个在哪里有提到? 谢谢