NO.PZ202112010200002401

问题如下:

An active portfolio manager seeking to purchase single-name CDS protection observes a 1.75% 10-year market credit spread for a private investment-grade issuer. The effective spread duration is 8.75 and CDS basis is close to zero.

What should the protection buyer expect to pay or receive to enter a new 10- year CDS contract?

选项:

A.The buyer should receive approximately 6.5625% of the notional.

The buyer should pay approximately 15.3125% of the notional.

The buyer should pay approximately 6.5625% of the notional.

解释:

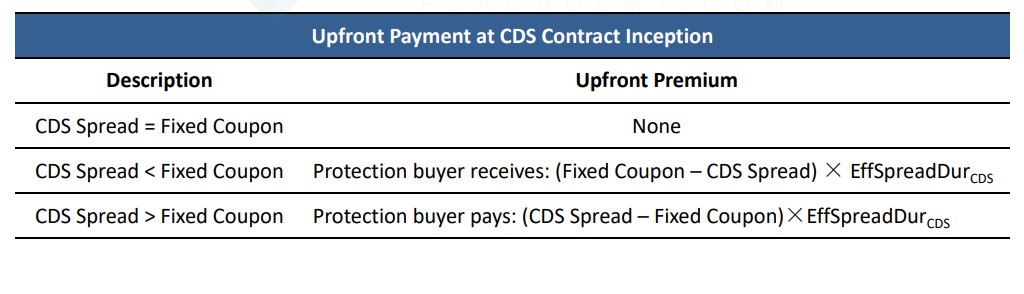

C is correct. Because the market premium is 0.75% above the 1.00% standard investment-grade CDS coupon, the protection buyer must pay the protection seller 6.5625% (= EffSpreadDurCDS × ∆Spread, or 8.75 × 0.75%) of the fixed notional amount upon contract initiation; the initial CDS price is therefore 93.4375 per 100 of notional with a CDS spread of 175 bps.

买CDS的人需要提前支付的金额=NP*(Fixed coupon -CD Sspread)*SD=NP(1%-1.75%)*8.75=-6.5625%NP。支付-6.5625%NP等于收到6.5625%NP。请问老师,哪里计算错了