NO.PZ2017092702000007

问题如下:

Given a €1,000,000 investment for four years with a stated annual rate of 3% compounded continuously, the difference in its interest earnings compared with the same investment compounded daily is closest to:

选项:

A.€1.

B.€6.

C.€455.

解释:

B is correct.

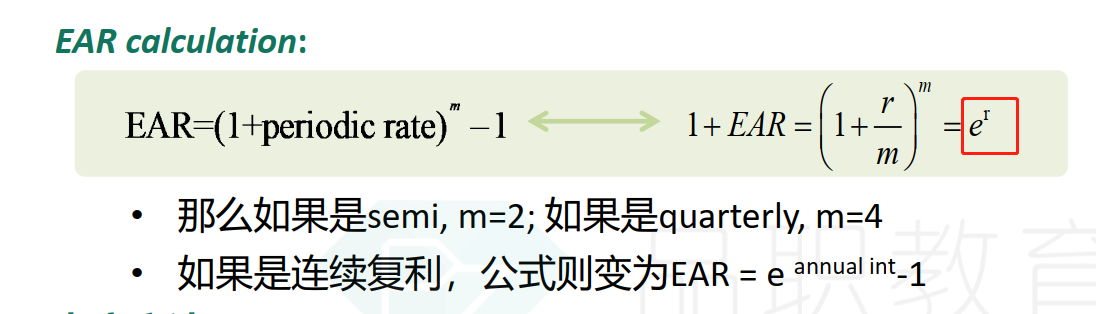

The difference between continuous compounding and daily compounding is

€127,496.85 – €127,491.29 = €5.56, or ≈ €6, as shown in the following calculations. With continuous compounding, the investment earns (where PV is present value) PVersN - PV = €1,000,000e0.03(4) – €1,000,000

= €1,127,496.85 – €1,000,000 = €127,496.85 With daily compounding, the investment earns: €1,000,000(1 + 0.03/365)^365(4) – €1,000,000 = €1,127,491.29 – €1,000,000 = €127,491.29.

根据不同的计息频率来计算两个利息。第一个是“.... compounded continuously”,第二个是“ compounded daily”,分别计算出利息后做差即可。

老师,compounding continuously求fv,用计算机是不是:n=4, i/y=3, pv=1,000,000 ,pmt=0, cpt fv?