问题如下图:

选项:

A.

B.

C.

D.

解释:

请问第二问的问题是什么意思?这里为什么需要做一个t-test,检验的目的是什么?谢谢~

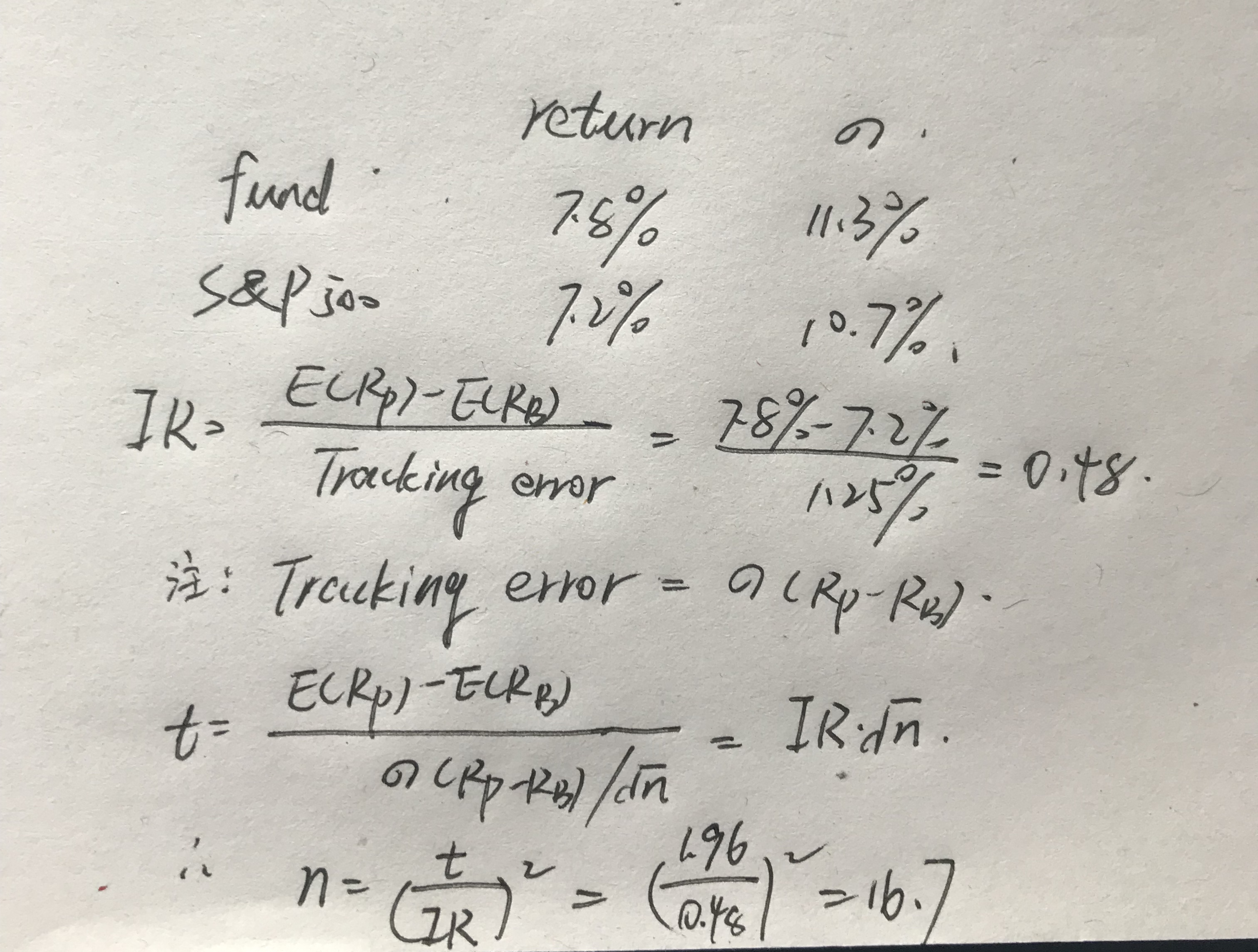

NO.PZ2016071602000001问题如下Over the past year, the HIR Funha return of 7.8%, while its benchmark, the S P 500 inx, ha return of 7.2%. Over this perio the funs volatility w11.3%, while the S P inx's volatility w10.7% anthe funs TEV w1.25%. Assume a risk-free rate of 3%. Whis the information ratio for the HIR Funanfor how many years must this performanpersist to statistically significant a 95% confinlevel?A.0.480 anapproximately 16.7 yearsB.0.425 anapproximately 21.3 yearsC.3.840 anapproximately 0.2 years1.200 anapproximately 1.9 yearsA is correct. The information ratio is (7.8 — 7.2)/1.25 = 0.48. Statisticsignificanis achievewhen the t-statistic is above the usuvalue of 1.96. Equation (29.5), the minimum number of years T for statisticsignificanis (1.96/IR)2 = 16.7. Note, however, ththere is no neeto perform the seconcomputation because there is only one correanswer for the IR question.老师, 想问一下 为什么 statistic有时用 1。96 有时候 1。645 ? 是默认 statisticsignifican就是 双尾吗 ?

NO.PZ2016071602000001问题如下Over the past year, the HIR Funha return of 7.8%, while its benchmark, the S P 500 inx, ha return of 7.2%. Over this perio the funs volatility w11.3%, while the S P inx's volatility w10.7% anthe funs TEV w1.25%. Assume a risk-free rate of 3%. Whis the information ratio for the HIR Funanfor how many years must this performanpersist to statistically significant a 95% confinlevel?A.0.480 anapproximately 16.7 yearsB.0.425 anapproximately 21.3 yearsC.3.840 anapproximately 0.2 years1.200 anapproximately 1.9 yearsA is correct. The information ratio is (7.8 — 7.2)/1.25 = 0.48. Statisticsignificanis achievewhen the t-statistic is above the usuvalue of 1.96. Equation (29.5), the minimum number of years T for statisticsignificanis (1.96/IR)2 = 16.7. Note, however, ththere is no neeto perform the seconcomputation because there is only one correanswer for the IR question.TEV/跟号N是标准误吗

NO.PZ2016071602000001问题如下Over the past year, the HIR Funha return of 7.8%, while its benchmark, the S P 500 inx, ha return of 7.2%. Over this perio the funs volatility w11.3%, while the S P inx's volatility w10.7% anthe funs TEV w1.25%. Assume a risk-free rate of 3%. Whis the information ratio for the HIR Funanfor how many years must this performanpersist to statistically significant a 95% confinlevel?A.0.480 anapproximately 16.7 yearsB.0.425 anapproximately 21.3 yearsC.3.840 anapproximately 0.2 years1.200 anapproximately 1.9 yearsA is correct. The information ratio is (7.8 — 7.2)/1.25 = 0.48. Statisticsignificanis achievewhen the t-statistic is above the usuvalue of 1.96. Equation (29.5), the minimum number of years T for statisticsignificanis (1.96/IR)2 = 16.7. Note, however, ththere is no neeto perform the seconcomputation because there is only one correanswer for the IR question.16.7是怎么出来的

NO.PZ2016071602000001 不懂第二个答案16.7年是怎么计算得到

NO.PZ2016071602000001 如果题目中没有说明到底是Jensen's alpha还是正常的alpha,而题目中求Jensen's alpha条件又齐全应该用哪种方法求呢?