NO.PZ2019042401000015

问题如下:

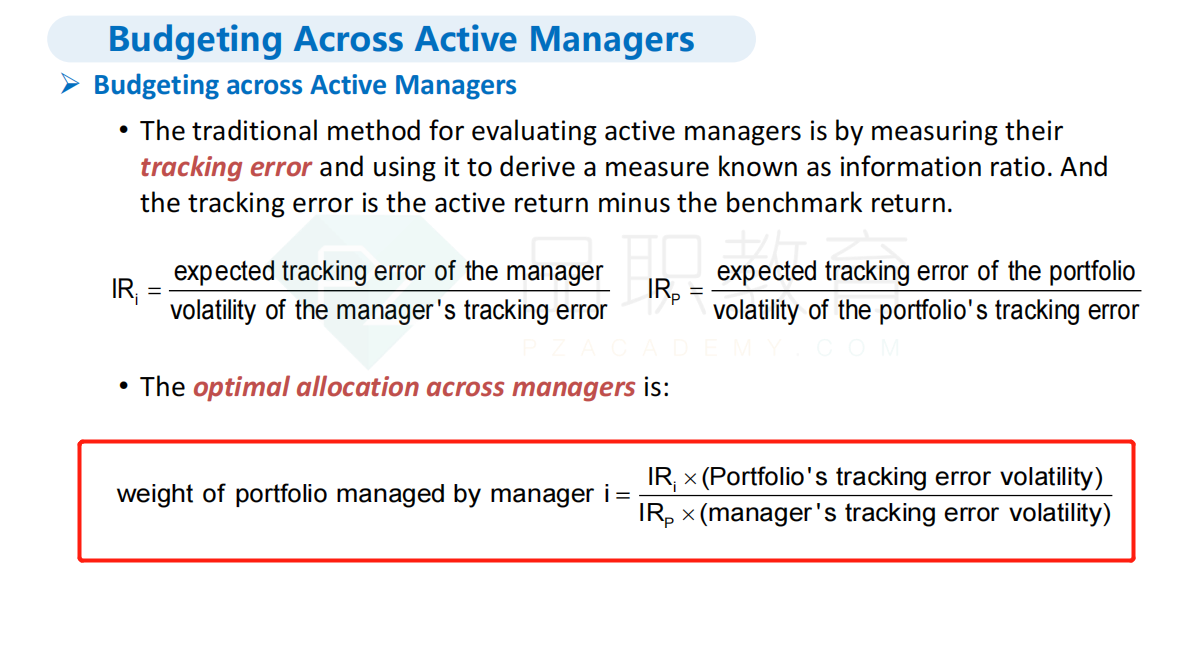

IRi is the information ratio of manager i and IRp is the information ratio of the total portfolio. Which of the following formulas represents the optimal weight managed by manager i ?

选项:

A. IRi×(manager’s tracking error)IRP×(portfolio’s tracking error)

B. IRp×(portfolio’s tracking error)IRi×(manager’s tracking error)

C. IRp×(manager’s tracking error)IRi×(portfolio’s tracking error)

D. IRi×(portfolio’s tracking error)IRp×(manager’s tracking error)

解释:

C is correct.

考点:optimal allocation across managers

解析:在基金经理之间进行最优资金配置时,应分配给manager i 的比例为 IRp×(manager’s tracking error)IRi×(portfolio’s tracking error)

要准确记忆公式。

请问这里的公式里的TE是不是要加上平方