NO.PZ201812020100000503

问题如下:

An upward shift in the yield curve on Strategy 2 will most likely result in the:

选项:

A.price effect cancelling the coupon reinvestment effect.

B.price effect being greater than the coupon reinvestment effect.

C.coupon reinvestment effect being greater than the price effect.

解释:

A is correct.

An upward shift in the yield curve reduces the bond’s value but increases the reinvestment rate, with these two effects offsetting one another. The price effect and the coupon reinvestment effect cancel each other in the case of an upward shift in the yield curve for an immunized liability.

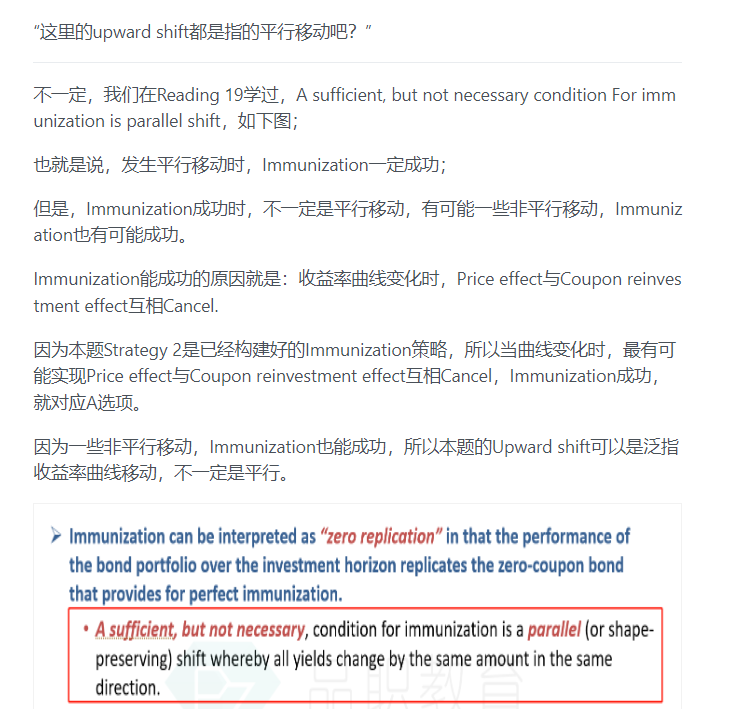

老师好 虽然说“对于Immunization的债券投资,其Price risk与Coupon reinvestment risk就能相互完全抵消。”这是个结论,但不是上课也说single liability 的duration match 里, 由于只考虑了 /假设平行移动,所以没考虑非平移动的情况。 也就是没考虑convexity (涨多跌少), 这里说upward slope(不一定是平移,就像截图里老师解释的一样) , 那就是说有可能是 非平移动, 如果有非平移动, 不是immunization 里就会有 structural risk . 这题为啥不说是coupon 涨 得 比 价格下跌的 大 所以选C? 谢谢。