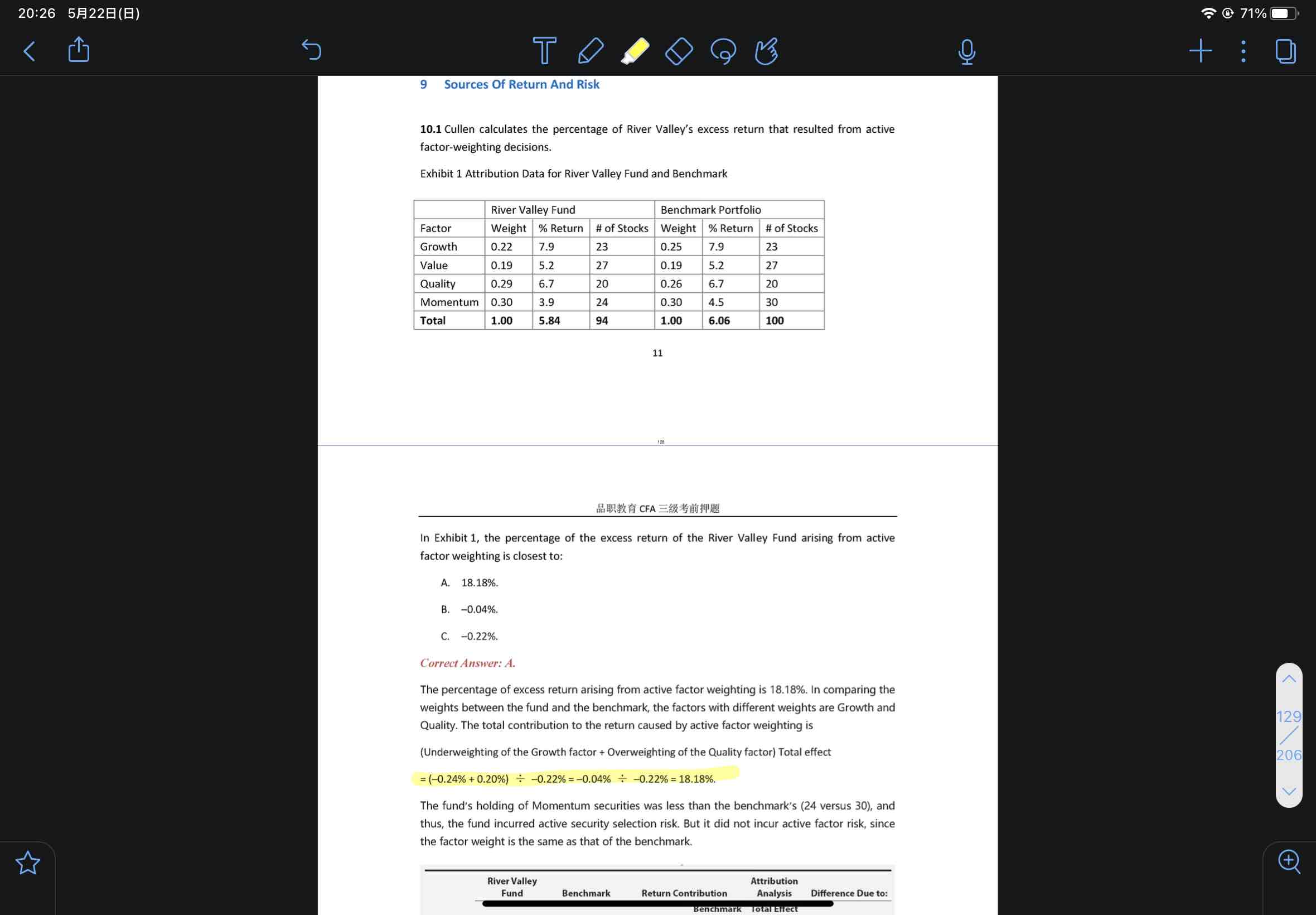

这里 -0.24为什么不应 (wi-wb)*(7.9-6.06) 而是直接*7.9

笛子_品职助教 · 2022年05月22日

嗨,努力学习的PZer你好:

区分equity里的收益归因和performance里的收益归因。

equity里的收益归因,是源自于equity例题,该例题就是这么写的。

return归因:(protfilio sector weight - benchmark sector weight )* benchmark weigth return.

也就是 (Wp - Wb)*Rb

后面在performance evualution这门课里,也会学到收益归因。equiy里的收益归因,是performance里的Brision model。不是performance里的macro model。

这两种归因方法都有各自的理由,都是正确的,只不过equity这门课只有Brision model一种方法。那么遇到equity的题目,就只能这么计算。

基础讲义85页。return归因:(protfilio sector weight - benchmark sector weight )* benchmark weigth return. (Wp - Wb)*Rb

----------------------------------------------虽然现在很辛苦,但努力过的感觉真的很好,加油!

梁 · 2022年05月22日

在考前发现这样一个坑谢谢老师