品职CFA错题本

写在前⾯的话:

临到考前,相信很多⼩伙伴在“预习”完那么多科⽬,会对⾃⼰产⽣怀疑,⽽且都会有经典的“两道题”是不会的。

分别是这道也不懂,那道也不懂。

ORZ。。。。

是不是这样就没救了呢?

当然不会啊。

虽然距离考试只有不到2周的时间啦,各位小伙伴们千万不要放弃治疗哦,品职CFA千人计划还在持续招募中,到22号的18:00截止哈(友情提醒一下:过期是无法参加的哦),如果需要了解的小伙伴请戳👇的链接哈。

除了品职千人计划以外,我们在考前还为⼤家订制⼀款新栏⽬-【品职CFA错题本】,发送⼀波精选的各科问题,⾥⾯会有助教们的总结分析,希望能给⼤家最后再捞点分。

毕竟错过的题,我们争取不要⼀错再错了哦。

今天让我们先来看看财务分析。

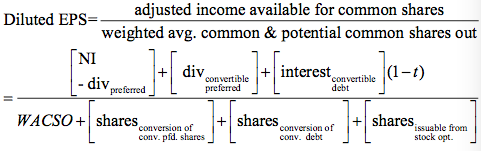

考点:Diluted EPS

精选问答1:

According to following information to calculate diluted EPS:

Net income is $1,650,000 in 2017

weighted average number of outstanding common shares are 1,000,000

preferred stock dividend is $200,000

25,000 stock options with exercise price of $20/share, average market price is $30/share, at the end of 2017, the price of stock is $18/share

A.1.57

B.1.43

C.1.30

答案:

B is correct.

Diluted EPS= (1,650,000-200,000) / (1,000,000+25,000-16,667) = 1.43, 16,667 = (25,000*20)/30

解析:

我们在计算Diluted EPS的时候,第一步应该先判断diluted security有没有稀释性,但是这个题只有一种潜在的可转换证券就是stock option,对于stock option它只会影响分母不会影响分子,所以我们可以判断一下stock option会不会增加股份数,也就是这个option会不会行权。

如果行权价格是大于市场的平均价格的,那stock option是不会行权的,所以不会影响分母,从题干的信息可以看出来行权价格$20是小于市场的平均价格$30的,所以肯定会行权,那我们可以用Treasury stock method, 这种方法是option转换成股票之后,意味着我们就是按照option里面约定好的价格购买了股票,相当于公司获得了这么多的融资资金,这些资金我们假设公司会用它来回购现有的股票,这里要注意的是回购价格是按照市场平均的价格来回购的,即可以回购(20*25,000)/30=16,667这么多股票,这是对分母的影响。

接下来我们计算DEPS,然后再和BEPS作对比。

那我们先写一下公式:

接下来我们一步一步来分析,先算分子,NI和优先股的DIV题干都已经给了,那就直接代入就是1,650,000 – 200,000

然后算分母,题干给了25,000的stock option,用库藏股的方法计算对分母的影响是增加股份数25,000-16,667=8,333这么多,然后再加上原来发行在外的1,000,000股,那么分母应该是1,008,333

所以最后计算结果是 1,450,000/1,008,333=1.43

我们再计算一下BEPS,公式如下:

因为DEPS < BESP, 即1.43 < 1.45, 所以由于stock option的行权,公司的蛋糕会被更多的人分,就会稀释现有股东的每股净利润,所以被稀释之后的EPS是1.43,所以选B。

易错点分析:

关于EPS的计算绝对是一级财务的重点,相信大家对公式的把握已经没问题了,但是如果因为一些陷阱丢了分那实在是太可惜了,比如这个题,有三个细节点大家需要注意:

第一点:为什么我们在计算DEPS的时候还要减掉preferred stock dividend?

相信很多同学有这样的问题,大家需要注意的是题干虽然有这个优先股的股利,但是这个优先股并不是一个潜在的可转换优先股,不属于diluted security,只是一个普通的优先股,所以对分子是没有影响的。如果这个优先股是convertible preferred stock,那我们就要考虑对分子的影响了。

第二点;行权价格,我们看的是一年的平均价格,年底的$18是干扰项。行权价格$20应该和$30比。

第三点:你要理解Treasury stock method,而且我们是按照市场的平均价格来回购的,题干给的期末价格是干扰项。

这三个细节点都掌握了,你才能做对这个题,所以基础知识一定要掌握好。

考点:Revenue recognizing

精选问答2:

Which of the following is an indication that a company may be recognizing revenue prematurely? Relative to its competitors, the company’s:

A.asset turnover is decreasing.

B.receivables turnover is increasing.

C.days sales outstanding is increasing.

答案:

C is correct.

If a company’s days sales outstanding (DSO) is increasing relative to competitors, this may be a signal that revenues are being recorded prematurely or are even fictitious. There are numerous analytical procedures that can be performed to provide evidence of manipulation of information in financial reporting. These warning signs are often linked to bias associated with revenue recognition and expense recognition Policies.

解析:

这个题是在说下面哪个指标的变化说明了这个公司是有可能提前确认收入的那我们分别分析一下三个选项:

A选项说的是是Asset Turnover是降低的,公式是Asset Turnover= Revenue/Average Total Asset, 如果提前确认收入,Asset Turnover变大还是变小是不一定的, 因为这个题只是在讨论对于AR的影响,而不是所有的Asset的影响,那你相对于你的竞争者,Asset肯定还有其他的变化,所以光讨论一个AR不足以推导出Asset Turnover的变化方向。所以不选A。

B选项说的是Receivables Turnover是上升的,公式是AR Turnover= Revenue/AR,由于提前确认收入,所以公司是收不到现金的,AR会增加,所以AR Turnover是下降的,所以B是错的。

C选项是DSO=365/AR Turnover, 是应收账款在外的天数,这里需要注意的是提前确认的收入是收不到现金的,所以会形成一个AR,你的这个AR相比你的竞争者就会上升,又因为AR Turnover= Revenue/AR, 分母变大,分数值是变小的,所以AR Turnover是下降的,所以DSO是上升的,所以选C。

易错点分析:

要想做对这个题需要注意2点:

第一点:你要知道提前确认的收入是收不到现金的,公司会记一笔AR,这个是大的原则

第二点:你需要知道每一个比率的具体公式怎么写,这就要求你掌握各个指标的计算公式。

考点:在建工程期间的利息资本化

精选问答3:

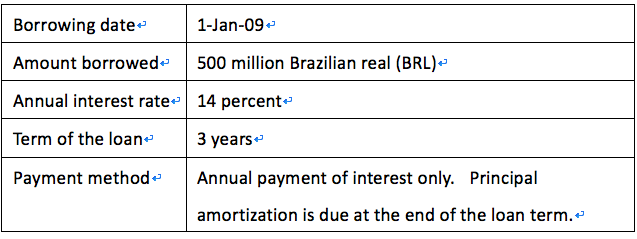

BAURU, S.A., a Brazilian corporation, borrows capital from a local bank to finance the construction of its manufacturing plant. The loan has the following conditions:

考点:在建工程期间的利息资本化

精选问答3:

BAURU, S.A., a Brazilian corporation, borrows capital from a local bank to finance the construction of its manufacturing plant. The loan has the following conditions:

The construction of the plant takes two years, during which time BAURU earned BRL 10 million by temporarily investing the loan proceeds. Which of the following is the amount of interest related to the plant construction (in BRL million) that can be capitalized in BAURU’s balance sheet?

A.130.

B.140.

C.210.

答案:

A is correct.

Borrowing costs can be capitalized under IFRS until the tangible asset is ready for use. Also, under IFRS, income earned on temporarily investing the borrowed monies decreases the amount of borrowing costs eligible for capitalization. Therefore, Total capitalized interest = (500 million×14%×2 years) – 10 million = 130 million.

解析:

不可否认的是惯性思维真的是很可怕,比如有一位同学看到这个题是这样计算的:

第一年利息:500 * 14% = 70

第二年的本金要扣除第一年已还的利息:500-70=430;

第二年的利息是420* 14% = 60.2

所以累计利息是:70+60.2=130.2 ≈ 130

-----------

如果再考虑到投资赚到的10m

总资本化利息应该是 130-10 = 120

其实这个计算是很正常也是正确的计算,但是在这个题里,有一个小的陷阱,协会给大家设定了一个Payment method,就是本金是最后一年一次性还的,所以每年要还的只有利息, Annual payment of interest only, 如果大家忽略了这个条件,那么后面的计算肯定会错。

所以在这个特定的情景下,正确的计算应该是第二年需要支付的利息为:本金500 million * 14%*2 -10 million=130

很多同学不理解这里为什么要减10,当我们把在建工程期间的利息资本化了之后,由于贷款这部分资金也可以产生收益,比如放在银行里就有利息,那么这部分利息收入就抵减了利息费用。

比如应该资本化的利息为100块,但本金放银行可以产生20块收入,那么真正需要资本化的利息费用是80

易错点分析:

第一点:读题没有读完整,审题不清

第二点:只有建造期的interest才资本化。虽然借款期有3年,但建造期只有两年,所以这里是乘以2,不是乘以3.

考点:资本化和费用化

精选问答4:

Companies X and Z have the same beginning-of-the-year book value of equity and the same tax rate. The companies have identical transactions throughout the year and report all transactions similarly except for one.

Both companies acquire a £300,000 printer with a three-year useful life and a salvage value of £0 on 1 January of the new year. Company X capitalizes the printer and depreciates it on a straight-line basis, and Company Z expenses the printer. The following year-end information is gathered for Company X.

Ending shareholders’ equity: £10,000,000

Tax rate: 25%

Dividends: £0.00

Net income: £750,000

Based on the information given, Company Z’s return on equity using year-end equity will be closest to:

A.5.4%.

B.6.1%.

C.7.5%.

答案:

B is correct.

Company Z’s return on equity based on year-end equity value will be 6.1%. Company Z will have an additional £200,000 of expenses compared with Company X.

Company Z expensed the printer for £300,000 rather than capitalizing the printer and having a depreciation expense of £100,000 like Company X. Company Z’s net income and shareholders’ equity will be £150,000 lower (= £200,000 × 0.75) than that of Company X.

ROE= Net income shareholder's/equity = 600,000/9,850,000 =0.61=6.1%

解析:

这个题是在说X和Z公司所有的业务都一样,除了对打印机的处理,X公司选择了资本化,每年计提折旧费用300,000/3=100,000。Z公司选择费用化,当年一次性计提费用300,000,所以Z公司的费用比X公司多300,000-100,000=200,000,扣除税之后,Z公司的NI比X公司少200,000*0.75=150,000.

X公司期末的所有者权益为10,000,000,Z公司比它少150,000,所以Z公司的Equity=10,000,000-150,000=9,850,000

易错点分析:

这个题计算分母Equity很简单,大家主要是计算NI的时候会犯错。

主要是因为很多同学不理解费用和税是什么关系,比如同样是100的收入,公司A的费用是60,公司B的费用是80,那么B的费用比A多20,那是不是B的利润就比A少20呢?

并不是的,在考虑所得税的情况下,假设税率为30%,A公司的NI=(100-60)(1-0.3),B公司的NI=(100-80)(1-0.3),我们可以看出B公司的NI比A公司少20(1-0.3)而不是20.

所以我们说费用相当于有一个税盾的作用。

考点:Gross VS Net Reporting

精选问答5:

An e-commerce company Sells hotel room nights on its Website Under agreement from a large number of major hotel chains. The hotel chains grant the company flexibility for the rooms they supply to the Company's website and for the prices charged.

These major chains bear the responsibility for providing all services once a customer books a room from the website. During 2011, the company received $5 million in payments from the sale of hotel rooms. The cost of these rooms was $4.5 million, which does not include $250,000 in direct selling costs. Under U. S. GAAP, the company’s cost of Sales is closest to:

A. $250, 000.

B. $4,500, 000.

C. $4,750, 000.

答案:

A is correct.

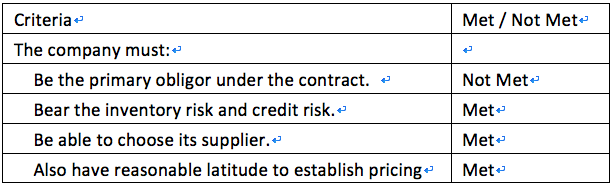

To report cost of sales under gross reporting (and include the cost of rooms), the company must meet four criteria:

The first criterion is not met. The major hotel chains have the obligation of fulfilling the room contract once it is entered into. Because not all of these conditions are met, the company must use net reporting, where revenue is $ 500,000 and cost of sales is $250, 000.

解析:

这个题是在说一个电子商务公司e公司,这个公司的业务是客户可以在它的网站上预定酒店,这个很像携程,所以这些酒店实际上是服务的提供者,和这个电子商务公司其实是没有关系的,2011年,这个e公司收到了5m的客户付的总的房费,e公司的成本是4.5m,相当于赚了0.5m,这个4.5m相当于e公司从那些酒店拿到的价格,可以了理解为进货成本,但是这个4.5m里面是不包含250,000直接的销售成本,就相当于是这个电子商务平台自己的成本,比如网站的维护费用,客服之类的成本。

然后题干问你e公司的COGS是多少?

这个cost的确认,有一个大的原则是match的原则,如果revenue的确认是net reporting,那cost的确认就只是平台的销售成本,而不应该包含从那些酒店拿到房间的成本,所以cost是250,000

如果这个题用的是gross reporting, revenue应该确认5 m, 成本就应该确认4.5m + 250,000,4.5m 相当于是进货的成本。

易错点分析:

这个题非常好,既考了你net reporting 和 gross reporting 的区别,还考了你cost的确认应该是基于一个match的原则,有一个判断错了你就做错这个题了。

而且这个题的答案还给你一个标准,就是如何判断是使用gross还是net,如果满足表格里的所有要求,就可以用gross reporting,只要有一条不满足,就只能用net reporting,这个大家可以当做结论来记一下。

好啦,一级财务分析的精选问答就到这里结束啦,最后再提醒一下哦,品职CFA千人计划还在持续招募中,到22号的18:00截止哈(友情提醒一下:过期是无法参加的哦),如果需要了解的小伙伴请戳下面的链接哈。