想问下老师currency over lay 在衍生品那一章节是用来外包然后产生超额收益的 为什么在权益这就变成了对冲风险的?外包到底是为了追求高收益还是为了对冲风险?

Q. Which of Parker’s statements about Manager B in Exhibit 1 is most appropriate? The statement about:

tracking errors.

excess return.

currency overlays.

Solution

B is correct. The comment about excess return being luck rather than skill is correct. Replication managers attempt to create a portfolio that tracks the performance and the volatility of the underlying index as closely as possible. The proper measure of skill is the tracking error: Manager B has the highest tracking error among the three managers.

A is incorrect because tracking error does not measure volatility of the portfolio; rather, it measures the volatility of the excess return between the index and the portfolio.

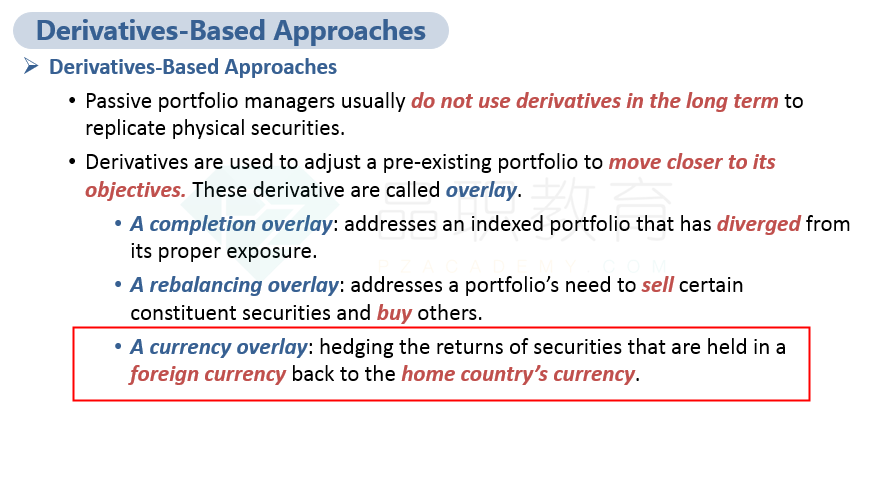

C is incorrect because a currency overlay assists a portfolio manager in hedging (not levering) the returns of securities that are held in foreign currency back to the home country’s currency.

Passive Equity Investing Learning Outcome

Discuss potential causes of tracking error and methods to control tracking error for passively managed equity portfolios