NO.PZ201710020100000106

问题如下:

6. Based on the exchange rate midpoint in Exhibit 1 and the rates in Exhibit 3, the 90-day forward premium (discount) for the USD/GBP would be closest to:

选项:

A.–0.0040.

B.–0.0010.

C.+0.0010.

解释:

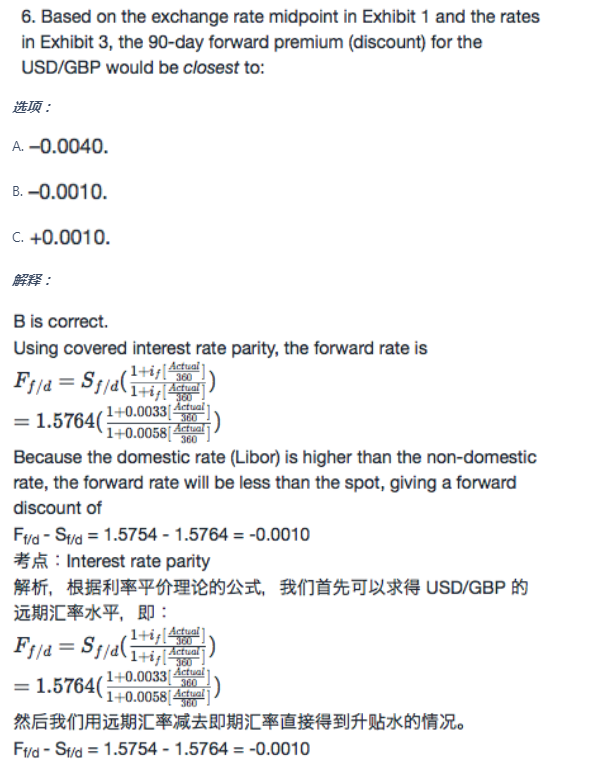

B is correct.

Using covered interest rate parity, the forward rate is

Ff/d=Sf/d(1+if[360Actual]1+if[360Actual])

=1.2303(1+0.0058[360Actual]1+0.0033[360Actual])

Because the domestic rate (Libor) is higher than the non-domestic rate, the forward rate will be less than the spot, giving a forward discount of

Ff/d - Sf/d = 1.2295 - 1.2303 = -0.0008

考点:Interest rate parity

解析,根据利率平价理论的公式,我们首先可以求得 USD/GBP 的远期汇率水平,即:

Ff/d=Sf/d(1+if[360Actual]1+if[360Actual])

=1.2303(1+0.0058[360Actual]1+0.0033[360Actual])

然后我们用远期汇率减去即期汇率直接得到升贴水的情况。

Ff/d - Sf/d = 1.2295 - 1.2303 = -0.0008

请问1.2295从哪里来呢?