NO.PZ201909280100000801

问题如下:

1 Based on Statement 1, Park should recommend:

选项:

A.hedge funds.

private equities.

commodity futures.

解释:

C is correct.

Real assets (which include energy, infrastructure, timber, commodities, and farmland) are generally believed to mitigate the risks to the portfolio arising from unexpected inflation. Commodities act as a hedge against a core constituent of inflation measures. Rather than investing directly in the actual commodities, commodity futures may be incorporated using a managed futures strategy. In addition, the committee is looking for an asset class that has a low correlation with public equities, which will provide diversification benefits. Commodities are regarded as having much lower correlation coefficients with public equities than with private equities and hedge funds. Therefore, commodities will provide the greatest potential to fulfill the indicated role and to diversify public equities.

理论上只要有收益都能抗通胀,但是题目是要最好的抗通胀和分散股票的效果。那真的是非commodity futures.莫属了。

这个图基本都解释了。虽然HF没有细说分散效果和抗通胀情况。没说代表的就是这方面不是很强,但是也有这方面的能力。然后是commodity futures,这个因为本身就是通胀指标之一,所以抗通胀效果是最好的。

还是进一步解释一下为什么PE和HF的抗通胀效果不怎么样,主要原因是抗通胀主要是指收益大于等于通胀。PE和HF中长期看是没问题的,但是问题是某个时期可能就不行,比如经济滞胀的时候,PE和HF(大部分的HF)和股市走势比较类似,都不好,但是物价却涨的很快。这个时候只有通胀指标是最好的,commodity 。

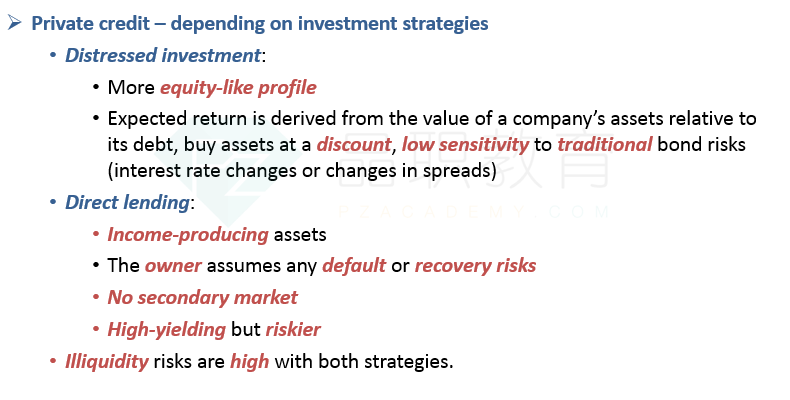

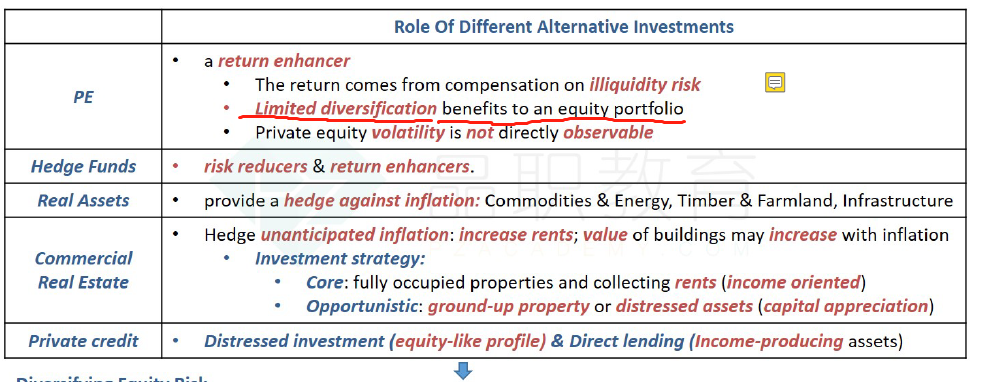

private credit里 截图里的两个 分别是啥意思 括号里的也没有理解