问题如下:

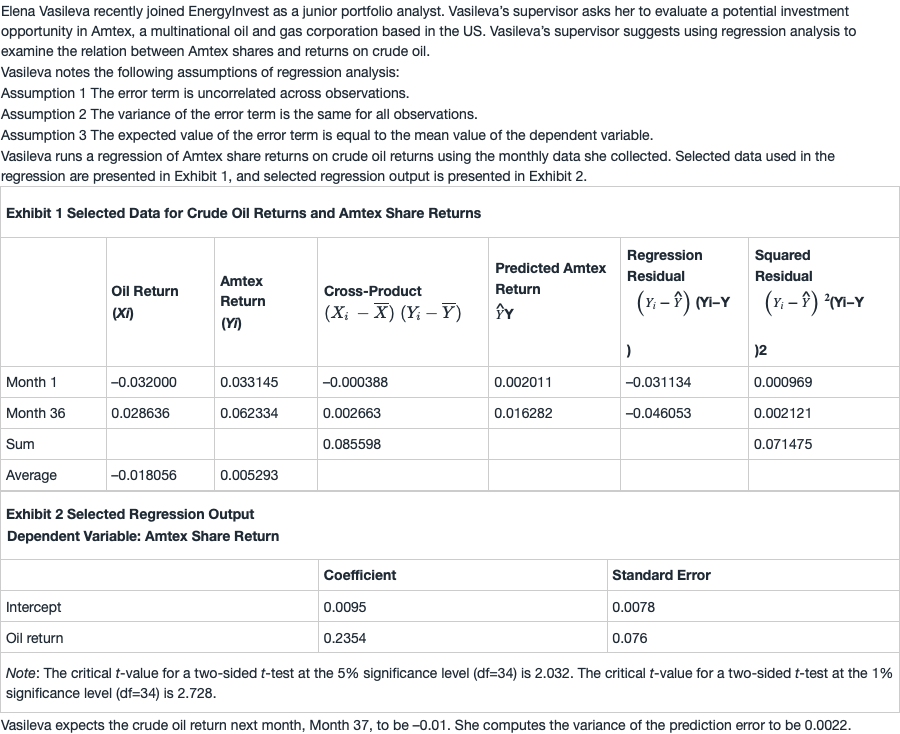

Based on Exhibit 2, Vasileva should reject the null hypothesis that:

选项:

A.the slope is less than or equal to 0.15

the intercept is less than or equal to 0

crude oil returns do not explain Amtex share returns.

解释:

C is correct. Crude oil returns explain the Amtex share returns if the slope coefficient is statistically different from zero. The slope coefficient is 0.2354 and is statistically different from zero because the absolute value of the t-statistic of 3.0974 is higher than the critical t-value of 2.032 (two-sided test for n – 2 = 34 degrees of freedom and a 5% significance level):

t-statistic =( 0.2354-0.0000)/

0.0760=3.0974

Therefore, Vasileva should reject the null hypothesis that crude oil returns do not explain Amtex share returns because the slope coefficient is statistically different from zero.

老师好,这题为什么B 不对? assume oil return = b2. h0: b2 < or = 0; ha: b2>0, T stat = 3.0974 > 2.032 and >2.728 所以拒绝原假设b2 小于或等于0 . 是不是因为 这里因为HA 是> 0 所以算T stat 的时候假设的value of b1 不等于0 ? 谢谢。