问题如下图:

选项:

A.

B.

C.

解释:

你好,请问可以照老师上课的画图和列公式方法解释一遍吗谢谢。

NO.PZ201903040100000104 有点难以理解这道题 考试会考这么难吗

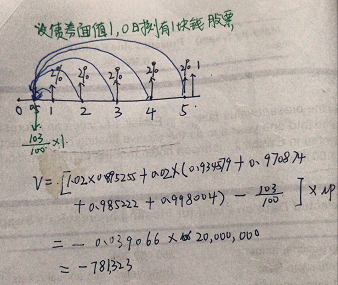

NO.PZ201903040100000104 -$781,323. -$181,323. B is correct. Te value of equity swis calculateVt=FB(C0)−(stst)NAEV_t=FB(C_0)-(\frac{s_t}{s_t})NA_E\\\\Vt=FB(C0)−(stst)NAE The swwinitiatesix months ago, so the first reset hnot yet passe thus, there are five remaining cash flows for this equity swap. The fair value of the swis terminecomparing the present value of the impliefixe rate bonwith the return on the equity inx. The fixeswrate of 2.00%, the swnotionamount of $20,000,000, anthe present value factors in Exhibit 5 result in a present value of the impliefixerate bons cash flows of $19,818,677: The value of the equity leg of the swis calculate(103/100)($20,000,000)= $20,600,000. Therefore, the fair value of the equity swap, from the perspective of the bank (receive-fixe pay-equity party) is calculateVt = $19,818,677 - $20,600,000 = -781,323老师,请问下,这里的0.02是怎么算出来的,为什么我算出来的是0.2,2%*20*1/2=0.2,好奇怪

我怎么觉得逻辑是[0.02*(0.5因子+1.5因子+2.5因子+3.5因子)+1*3.5因子-103/100]*NP,但上面画图题中确是[0.02*(0.5因子+1.5因子+2.5因子+3.5因子)+1.02*0.95255-103/100]*NP,为什么是1.02*0.95255?

请问这个折现的计算为什么可以按单利,题目没有明确说明呀?