NO.PZ2024030506000064

问题如下:

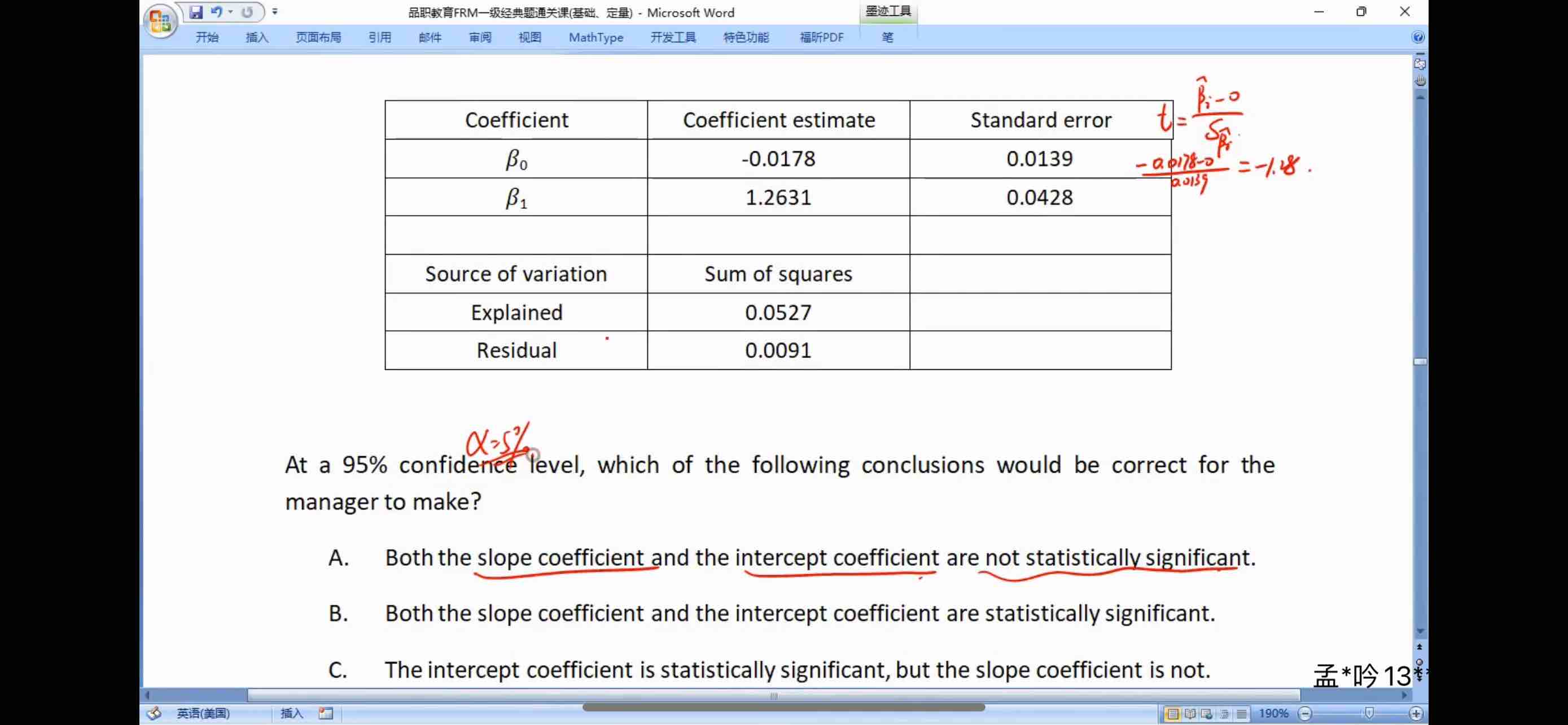

A market risk manager is analyzing the performance of VTFX, a large cap growth

mutual fund that uses the performance of the MSCI World Large Cap Growth Index

(MWG) as a benchmark. The manager runs a regression using monthly returns of

VTFX as the dependent variable and monthly returns of the MWG as the

explanatory variable. The constructed regression model and the results of the

regression are as follows:

𝑉𝑇𝐹𝑋𝑡 = 𝛽0 + 𝛽1(𝑀𝑊𝐺𝑡) + 𝜀t

At a 95% confidence level, which of the following conclusions would be correct for the manager to make?

选项:

A.

A. Both the slope coefficient and the intercept coefficient are not statistically significant.

B.

B. Both the slope coefficient and the intercept coefficient are statistically significant.

C.

C. The intercept coefficient is statistically significant, but the slope coefficient is not.

D.

D. The slope coefficient is statistically significant, but the intercept coefficient is not.

解释:

D is correct. In implementing a t-test with a 5% level of significance, the test statistic value is compared to the critical values from a standard normal distribution.

The test statistic for the slope coefficient is given by 𝑇 = (𝛽1−𝛽0) / 𝑠.𝑒.(𝛽1) = (1.2631-0)/0.0428 = 29.51.

Similarly, the test statistic for the intercept coefficient is calculated as (-0.0178-0)/0.0139 = -1.28.

Since the critical value from a standard normal distribution is 1.96, only the slope coefficient can be concluded as being statistically significant. The intercept term is not statistically different from zero at the 5% level of significance.

A, B, and C are incorrect.

Section: Quantitative Analysis

Learning Objective: Construct, apply, and interpret hypothesis tests and confidence intervals for a single regression coefficient in a regression.

Reference: Global Association of Risk Professionals. Quantitative Analysis. New York, NY: Pearson, 2022. Chapter 7. Linear Regression

老师,这道题计算出结果后,如果查表,b0的检验统计量是1.28,b1的统计量是29.51,是用t分布表吗?横轴看0.05,纵轴的自由度怎么看呢?