老师你好,这道题目中用到的两个公式在讲义哪里?另外为什么讲解中公式里用的是residual risk 而讲义上写的是active risk volatility?

DD仔_品职助教 · 2023年11月17日

嗨,从没放弃的小努力你好:

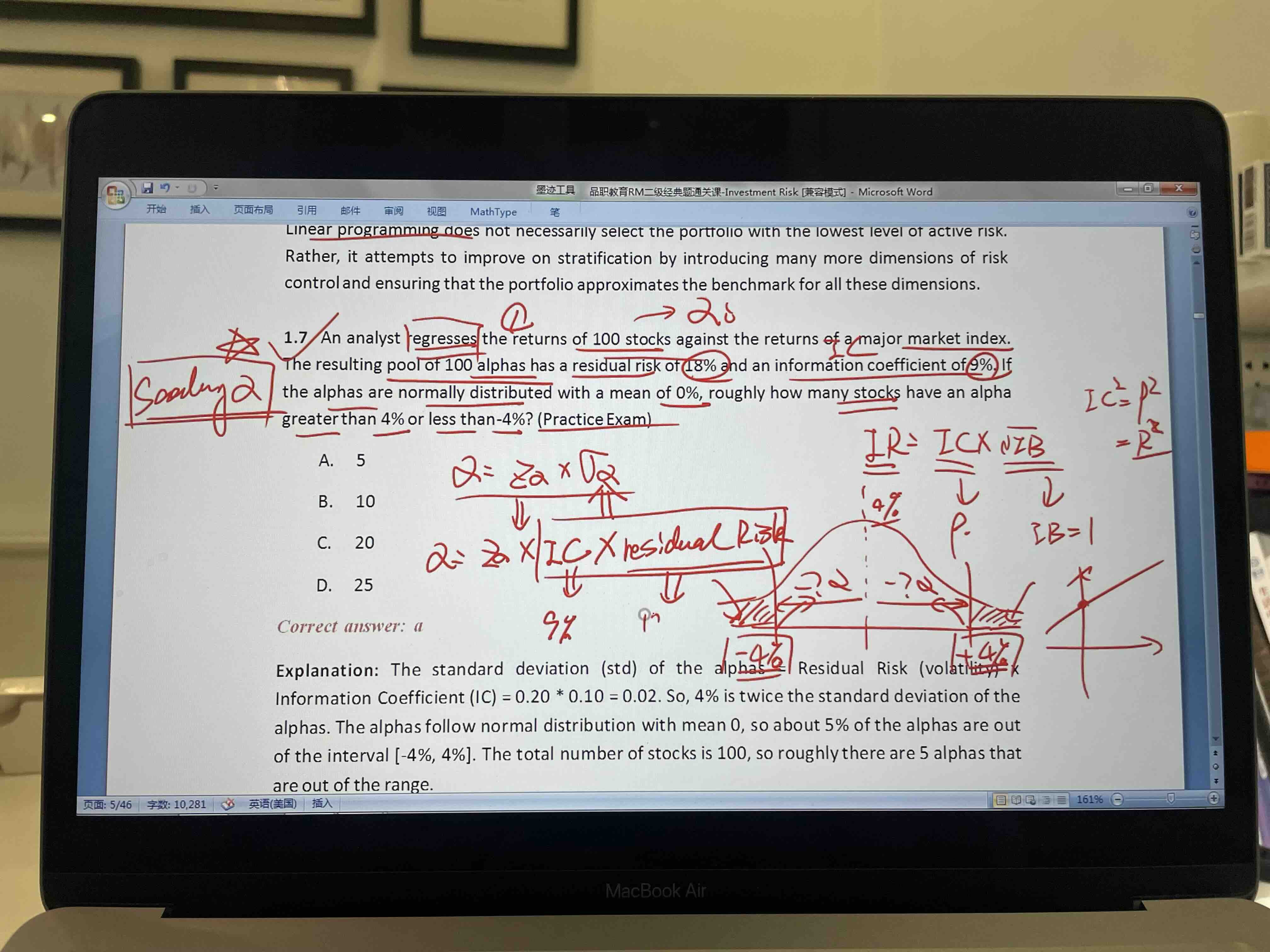

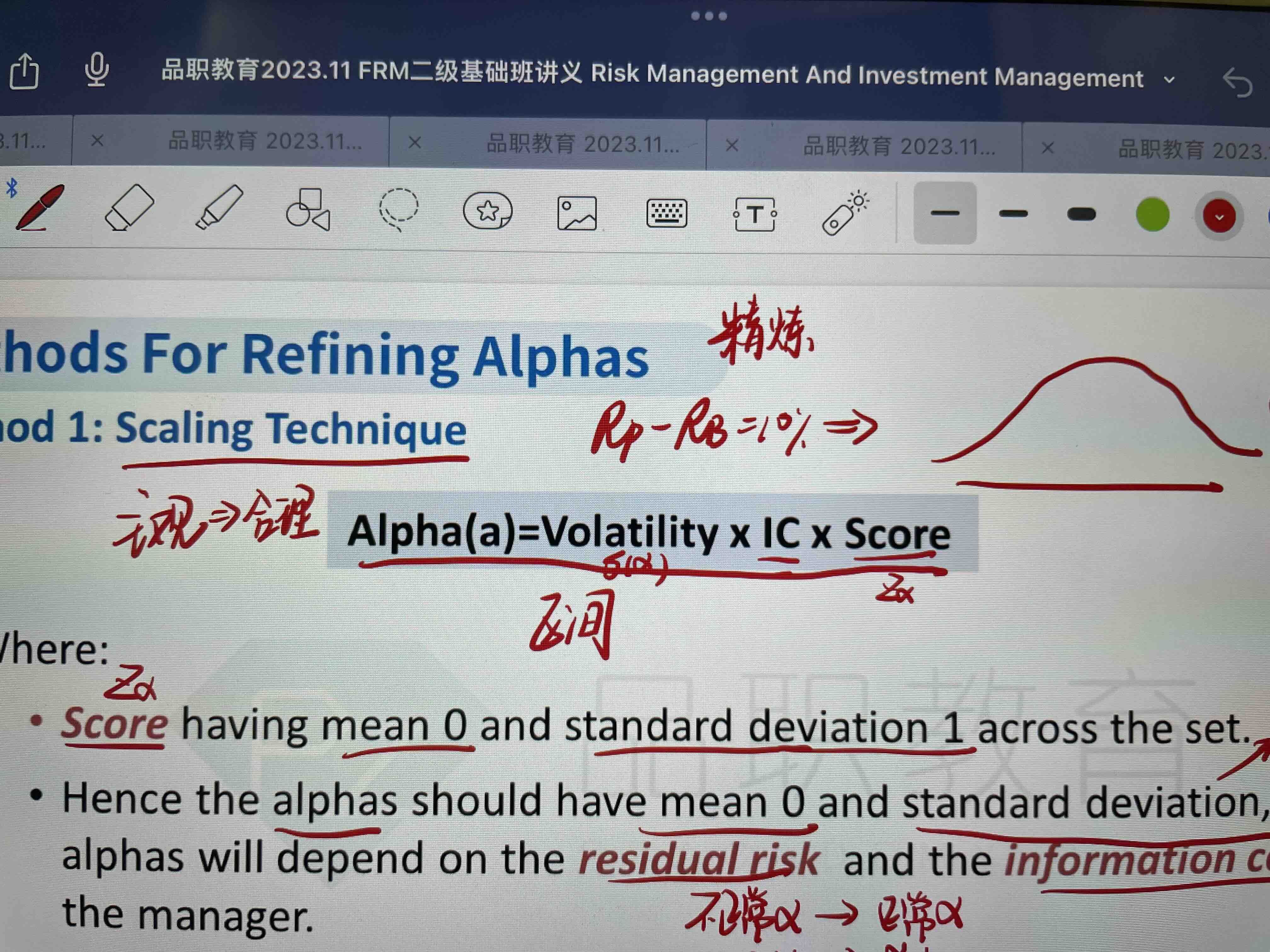

alpha=Z*standard deviation of alpha

这是因为alpha经过正态分布标准化满足了正态分布,均值为0,所以有这个式子成立。

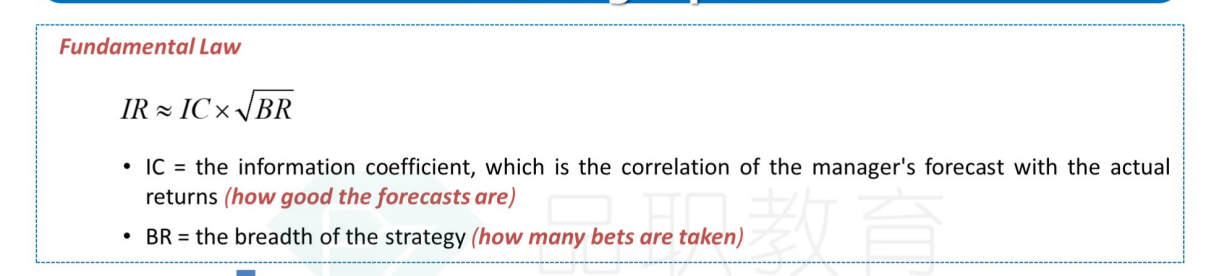

右边的公式是fundamental law:

The active risk of an investment or a portfolio is the difference between the return and the benchmark index's return for that security or portfolio. 通常用tracking error来衡量,在实务中大多数时候用alpha的标准差来衡量。

residual risk比较复杂,举个例子Suppose a portfolio of investments has a standard deviation of 15% and the systematic risk is known to be 8%. The residual risk would be equal to:15%-8%=7%,你就把理解成题目里说的volatility就行了,原版书也没有展开。

alpha的标准差等于residual risk 乘以IC。

----------------------------------------------加油吧,让我们一起遇见更好的自己!