NO.PZ2019010402000013

问题如下:

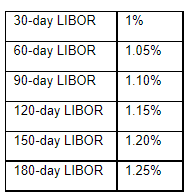

A bank entered into a 3×6 FRA 30 days ago as a fixed receiver. The fixed rate is 1.25%, and notional principle is $100 million. The settlement terms are advanced set, advanced settle. The current Libor data is as follows:

The value of this 3×6 FRA is:

选项:

A.

11,873

B.

-11,873

C.

-12,579

解释:

B is correct.

考点:FRA的估值

解析:

画图:

题中的银行是fixed receiver,即FRA的short方。上图是以Long方,即Borrower(floating receiver)为例,所以fixed receiver (short)的value=-long=-11873

为什么FRA是1.25